As access to alternative investments and private markets expands, financial advisors can expect more clients to ask about how they fit into portfolios, whether out of sheer curiosity or with a request to incorporate them into their portfolios. With that comes education. Advisors need to be prepared to help clients understand the potential benefits and the very real limitations of alts, to identify who is best suited for these types of strategies within a broader portfolio.

8 steps to talking about alternatives with your clients

When we introduce alternative investments, our goal isn’t to steer clients toward a particular product. It’s to help them understand whether these strategies practically align with their goals, preferences, and constraints. The most effective conversations are grounded in careful listening, education, and a disciplined evaluation process.

- Begin with the client’s situation, not with solutions

Start by understanding what’s prompting the conversation. Are they expressing concerns about concentrated exposure? Do they have questions about volatility? Interest in accessing different sources of return? This clarity helps us determine whether alternatives are even worth exploring—not every client needs to be pointed in that direction. - Use familiar portfolio concepts as a foundation

Many clients think about their portfolios in terms of growth (equities) and stability (bonds). Position alts simply as potential additional building blocks that may address specific needs. This isn’t about abandoning the 60/40 framework—it’s about providing context so clients can decide whether additional tools are appropriate for them. - Address key considerations up front—especially liquidity, valuation and fees

For clients evaluating alts, four questions consistently emerge:

• Liquidity: “How often can I access my money?”

• Valuation: “Will I get daily, monthly, or quarterly valuations and will they be market-based or fair-based?

• Fees: “What costs should I expect?”

• Complexity: “Will I be able to understand this?”

Set expectations early, particularly around illiquidity and fees, so clients can make an informed decision about whether these characteristics align with their comfort level and time horizon

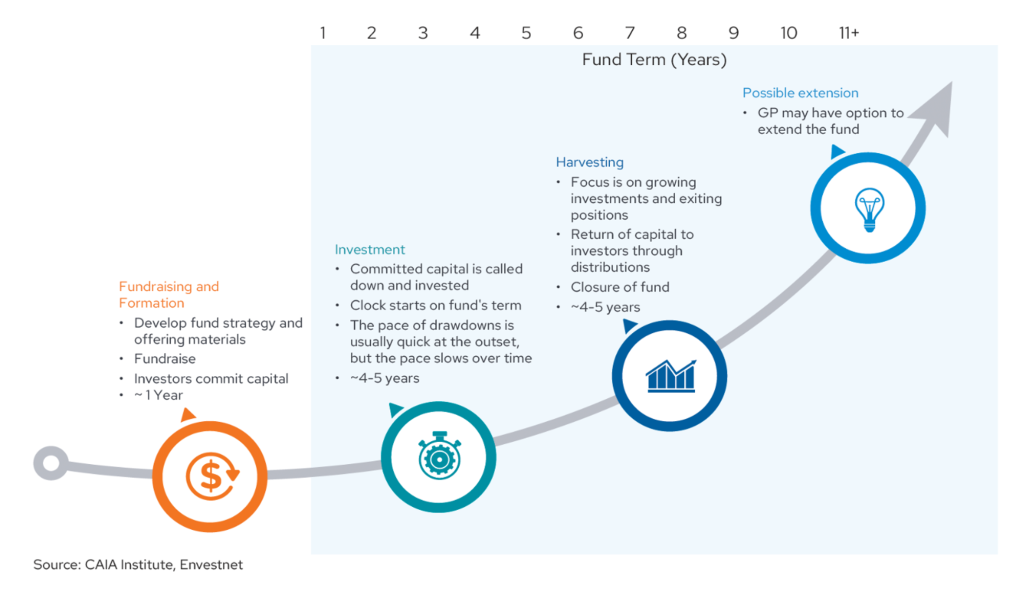

The lifecycle of a private market fund could be 10 years or more

- Translate concepts into everyday language

Alternatives can feel abstract. Use plain-language examples to help clients understand the underlying economic activity. For instance, instead of referencing “private credit,” explain that some strategies involve lending to established businesses. The goal is clarity, not persuasion. - Consider a measured approach if the client appears suitable

When a client’s situation suggests that alts might be appropriate, a small initial allocation can be a prudent way to assess comfort and portfolio fit. This step is always about testing suitability, not encouraging participation. - Provide context without exerting pressure

It can be helpful to share how other clients in similar circumstances have approached the decision—without implying that those choices should dictate someone else’s. Context can normalize the discussion while keeping the focus on the individual client’s needs. - Emphasize your due-diligence process

Rather than highlighting return potential, walk clients through how alternative strategies are evaluated, risks are assessed, and fit is determined. A disciplined process reassures clients that any consideration of alts is grounded in rigor, not trend-following. - Clarify next steps, even if the next step is “pause”

Every conversation should end with a clear plan—whether that’s gathering more information, reviewing educational material, updating the client’s financial plan, or deciding that alternatives aren’t the right fit at this time.

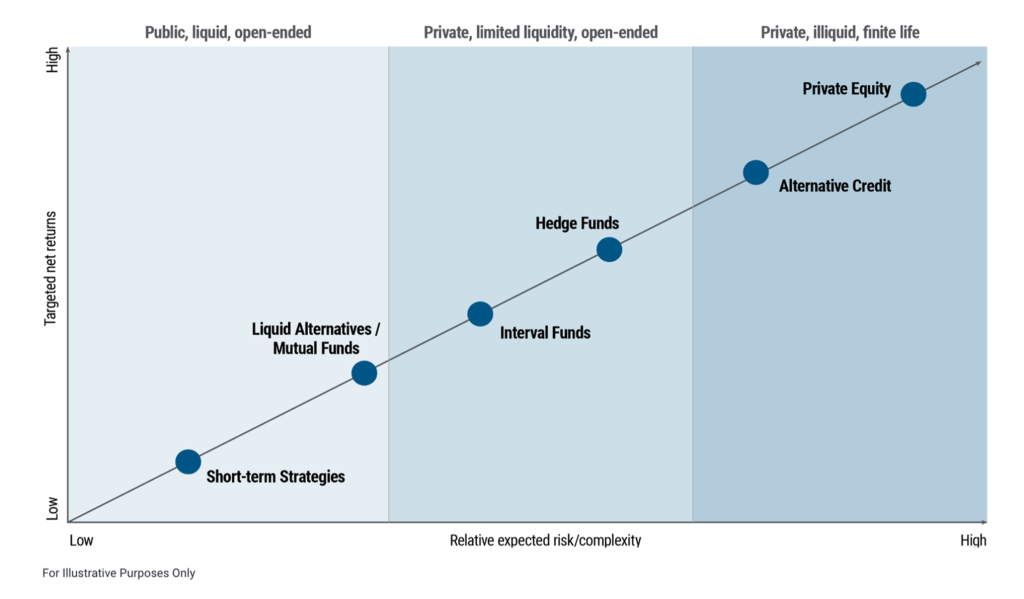

A visual representation of variables to consider for various options can be really helpful in these conversations.

These conversations are important

"At Envestnet, our vision is to unify a historically siloed alternatives universe, so that these asset classes no longer feel like 'alternatives.' By automating burdensome workflows, and adding transparency and clarity to portfolio performance, we can level the playing field for advisors in accessing and integrating private markets. This opens up a whole new world of opportunity for strengthening client portfolios by adding diversification and offering greater return and income potential."

Dana D'Auria, CFA, Co-Chief Investment Officer and Group President, Envestnet Solutions

Alternative investments aren’t a passing trend, but that doesn’t mean they’re right for every client. Depending on a client’s liquidity needs, risk tolerance, and time horizon, alternatives may play an important role in a thoughtful, well-constructed portfolio. Our responsibility is to help evaluate those factors carefully and introduce alts only when they align with the client’s goals and preferences.

Advisors who build the expertise to assess and explain these strategies will be well-positioned to support clients as interest in alternatives continues to grow. The question isn’t simply whether alternatives will become more common across wealth management; it’s whether you’ll have a clear, disciplined approach in place when clients want to understand how (or if) they fit into their plan.

Curious how interval funds bridge the gap between public and private markets? Read our introductory guide.