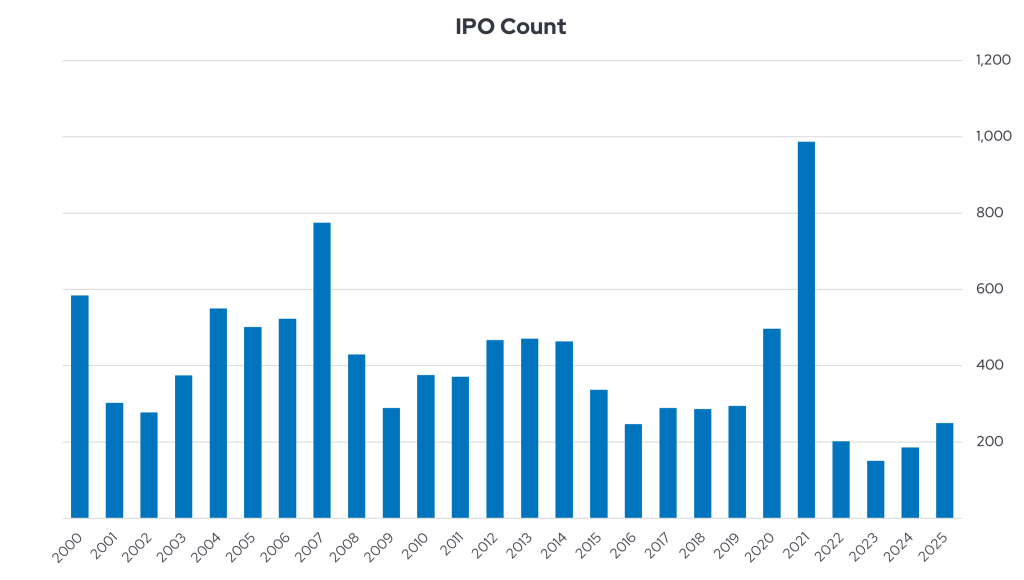

In the post-COVID world, companies have been staying private longer rather than rushing to go public as quickly as they did around the turn of the century. In 1999, the median IPO happened about 5 years after founding. In 2025, the median corporation was 12 years old at IPO.1 The sheer amount of private equity and venture capital available to businesses has enabled this trend. When a firm can raise tens of billions of dollars privately, there is less urgency to list its shares on the stock exchange. Other than the special purpose acquisition company (SPAC) boom of 2021, U.S. IPO activity has been relatively restrained in recent years. Figure 1 illustrates this shift.

Despite the slowdown in IPOs since the SPAC fever broke, no capital market is as deep, liquid, or prestigious as the U.S. stock market. Going public also allows investors and employees to cash out more easily. In short, an IPO is a positive event.

The mega IPO wave in 2026

Space Exploration Technologies (SpaceX), OpenAI, and Anthropic are forecast to go public this year, although only SpaceX and Anthropic have filed S-1 filings with the Securities and Exchange Commission. SpaceX is expected to debut first, with OpenAI and Anthropic potentially following later in the year. OpenAI and Anthropic will likely wait until the autumn for their own IPOs. SpaceX is reportedly seeking to raise $75 billion at a valuation of nearly $1.8 trillion.2 If achieved, this would make it the largest IPO in history. Figure 2 shows previous mega IPOs for context.

SpaceX’s desired valuation would make it one of the largest public companies in the U.S.3 Anthropic ($965 billion valuation) and OpenAI ($852 billion valuation) would rank among the top 15 most valuable U.S. publicly traded companies if they issue shares at their present valuations.4 Based on experience, we also know that valuations often climb during the IPO process.5 Regardless, these companies will expand investor access to AI-themed equities and reshape the investment landscape.

In total, SpaceX, OpenAI, and Anthropic will likely launch some of the largest IPOs ever, potentially worth a combined $3.5 trillion or more. This scale of issuance would meaningfully reshape equity markets.

“Digesting” these large issuances will not be easy for Wall Street, but demand for shares will probably still well outpace the supply of these stocks. How might investors and their advisors be affected by this wave of IPOs? Let us consider the possibilities for both active and passive investment strategies.

Viewing IPOs through two lenses: Active and passive

For active managers, the decision is relatively simple: Do you allocate, and at what size?

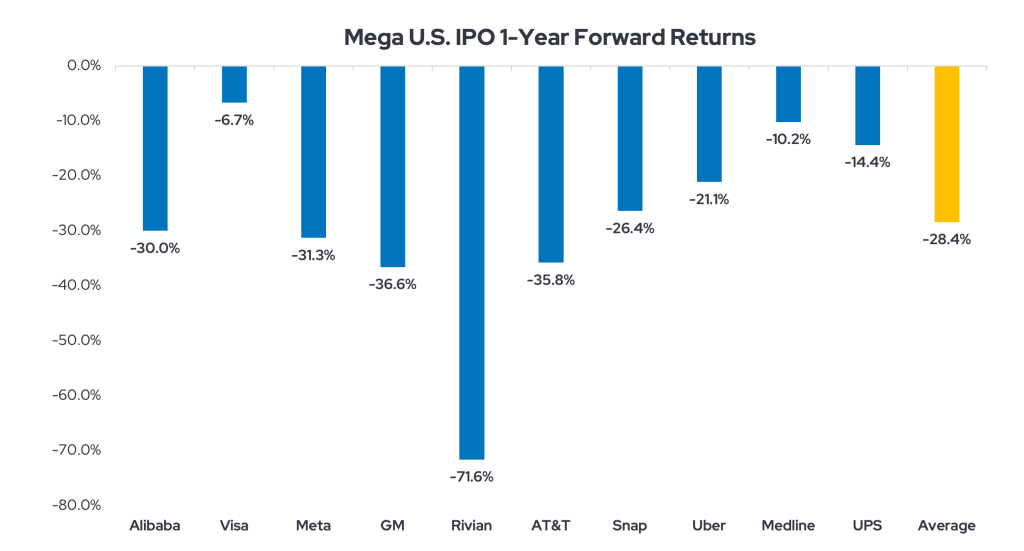

The historical data warn against expecting strong short-term returns, although longer-term returns are not so disappointing for many of these stocks.

Figure 3 shows that large IPOs often disappoint over the first 12 months.

For equity market indices, and the passive funds that follow them, the way forward is less straightforward. Index construction is more subjective than many investors realize. In fact, index rules are often quite subjective in nature. On April 30, 2026, S&P Dow Jones Indices (S&P DJI) actually decided to ask market participants what to do about mega IPOs:

S&P DJI has been actively monitoring the anticipated initial public offerings (“IPOs”) by companies with unprecedented market capitalizations often referred to as “MegaCaps.” S&P DJI defines a “MegaCap” company as one with a total company-level market capitalization equal to or greater than the 100th largest company in the S&P Total Market Index (TMI). In 2026, some U.S. MegaCap companies may conduct IPOs. Additionally, certain U.S. public companies have reached or may reach MegaCap status without positive net income from continuing operations.

These MegaCap companies may pose unique challenges for index methodologies within the Relevant Index Families, which were originally designed for more conventional listing profiles. MegaCap IPOs have the potential to achieve immediate and material investor ownership, trading liquidity, and market relevance, yet adherence to the existing index eligibility rules could prevent such IPOs’ timely index inclusion and impact the overall index’s effectiveness as a benchmark.

Through this consultation, S&P DJI is seeking feedback regarding whether the proposed, narrowly defined rule exceptions for MegaCap companies and adjustment to the IPO seasoning period would enhance the continued ability of the subject indices to reflect the investable market universe while maintaining the core principles of transparency, consistency, and replicability that underpin S&P DJI index construction.6

Most notably, S&P DJI was considering whether to waive the requirement for “MegaCaps” to be profitable and whether to shorten the twelve-month post-IPO seasoning period to six months for MegaCaps. These possible changes were ultimately not implemented, though. The Nasdaq-100 has already reduced its seasoning period to just fifteen days through a new “fast entry” rule.7 With $662 billion in exchange-traded funds indexed to the Nasdaq and $11.8 trillion in passive assets indexed to the S&P 500, index rules are important.8 Since around 24% of the S&P 500’s market capitalization is held by passive products, their behavior is significant.8

Much depends on float size and lockup structure. (In this context, “float” refers to the shares of a stock available for transactions on the open market and not bound by trading restrictions.)

Index funds may face liquidity constraints when attempting to track benchmarks that include these stocks. SpaceX plans to initially float about 5% of its shares, with more shares floating after a six-month lockup. This may create a supply-demand imbalance for products tracking the Nasdaq-100 because they would have just fifteen days to acquire enough SpaceX stock to match its index weight.

The same pattern is likely to repeat itself, to some extent at least, when Anthropic and OpenAI debut. Following each major IPO, passive investors will almost certainly have less time between share issuance and index inclusion than normal. Individual investors and active portfolio managers will compete for newly issued shares, with index products essentially forced to buy these stocks regardless of price. These situations may cause significant price volatility in SpaceX, OpenAI, and Anthropic stocks, as well as in the funds that quickly acquire shares of these companies. Short-term price spikes in SpaceX, OpenAI, and Anthropic may thus be especially noticeable when each stock is added to a major equity market index. Over time, however, more shares of these stocks will float.

Research from Goldman Sachs indicates that large firms with extremely small IPO floats—issuing 7% or less of their shares to the public—typically see their floats rise to about 54% of shares outstanding within two years. Across its broader IPO dataset, the average company that began trading with roughly 24% of shares available publicly had increased that figure to 69% after a two-year period.9 While many stock market indices adjust constituent weights based on freely floating shares, we remain cognizant of the tremendous size of these IPOs. The unprecedented amount of equity entering the public markets and the adjusted index rules governing the inclusion of these stocks could cause volatile trading.

The Bottom Line for Advisors

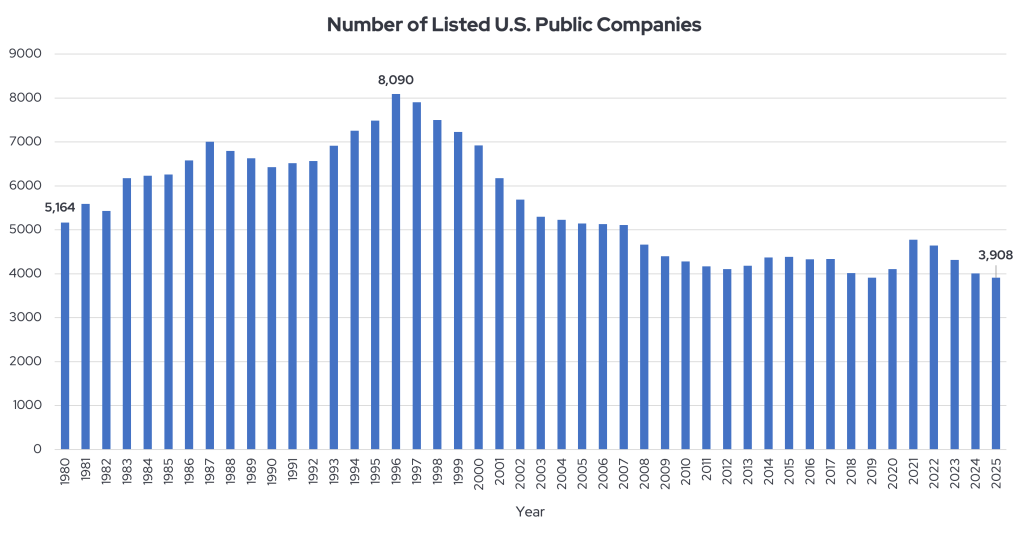

Figure 4 illustrates that the number of U.S. public companies has been shrinking for many years.

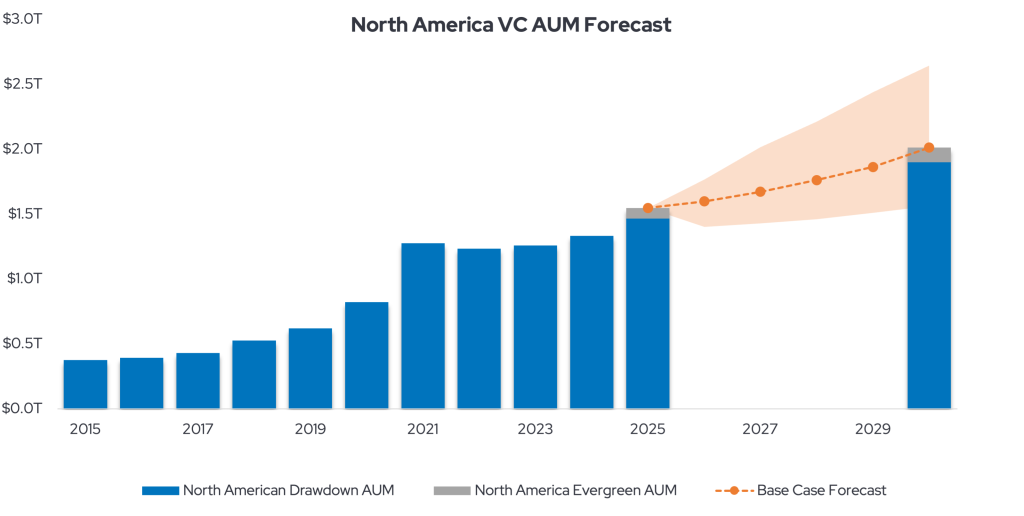

Figure 5 shows that venture capital assets under management (AUM) are forecast to climb.

This convergence of forces may continue to create conditions for fewer but larger IPOs. In this scenario, venture capital investors incubate private companies for longer until public markets welcome mega IPOs into an investor base hungry for new issues. Mega IPOs are not outliers—they may represent a lasting shift in how companies enter public markets. They are potential heralds of a coming mega IPO trend.

Stay ahead of market trends on our blog.