Rewarded risk factors are recognized as a fundamental component of equity returns. Envestnet | PMC believes that the most robust among the studied risk factors are value, momentum, quality, low volatility, and size. Like all return components, factors are cyclical in nature. Below, we take a look at the performance of these factors in the current market environment.

How factors have fared

Stock prices were mostly higher in the quarter following the first quarter’s mixed results. However, as in the first quarter there was a significant amount of dispersion in returns, with certain sectors advancing more than 17%, while others declined more than 2%. The economy’s resiliency has surprised many investors and analysts, and the strength in stock prices seems to be suggesting that the U.S. economy may avert a recession. International stocks generated positive results during the quarter, and generally were in-line with U.S. equities.

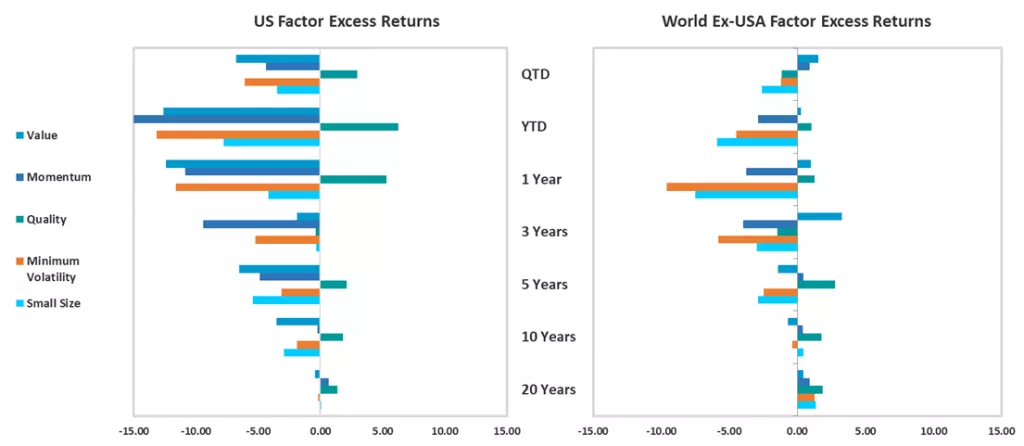

Relative performance across U.S. factors was narrower this quarter than in the first. Nearly all factors posted losses relative to the market capitalization benchmark. Ex-U.S. factors fared slightly better, with more modest losses or slight gains.

- Value investors likely suffered whiplash during the first half of 2023. After staging a breathtaking comeback against growth in 2022, value’s remarkable underperformance year-to-date means it has given up all of the relative ground it made up last year, and then some. Some of this is a sector story, as investors rotated to quality stocks in growthier sectors while avoiding value-leaning bank stocks after the mini-banking crisis earlier this year. But there are more chapters to this book. For more thoughts on what may be contributing to the wild ride for value, see this quarter’s Factor Insights piece.

- Quality continues to benefit from an uncertain market environment. Despite the somewhat befuddling resilience of the domestic economy, the risk of a hard landing remains. As a result, investors have flocked to relative safety in companies with strong balance sheets, boosting growth sectors like technology (and particularly the largest companies within this sector). Though quality posted a slight loss in ex-U.S. equity markets this quarter, it is one of only two positive factors year-to-date there.

- Small caps felt the sting of the other side of the quality trade. These stocks tend to have weaker balance sheets relative to their large cap counterparts, and sell off in a rotation to quality.

- Momentum has struggled the most in the U.S. in the face of whipsawing market leadership. Domestic momentum strategies ended 2022 with a heavy value bent, and that positioning was a collossal drag in an environment that favored growth. Those strategies that rebalance on a periodic basis underwent a massive rebalancing during the first half, as they rotated back to technology and other growth-oriented sectors. The MSCI USA Momentum Index saw turnover of nearly 70% in June.

- Minimum volatility tends to lag in strong uptrending markets, as the factor is inherently biased toward low beta. While it has historically had a positive correlation with the quality factor, it performs best in highly risk-averse environments with negative or more modest gains in the broad market. Over the long term, this factor’s primary purpose is to reduce portfolio volatility and enhance diversification.

The rough patch for many factors has affected trailing periods observed at this point in time. However, it is important to remember that the observation is just that—a point in time. Factor performance is cyclical, just as it is for all assets, as factors bear the effects of both the macroeconomic, business, and sentiment cycles. As building blocks of equity returns, the case for factors over the long-term remains unchanged, but requires patience to ride out these short-term cycles.